DDR4 End of Life: Samsung, Micron & Renesas EOL Impact on Industrial Memory (≤70 chars)

The Great DDR4 Sunset: How Samsung, Micron, and Renesas EOL Waves Are Reshaping Industrial Memory Procurement Through 2027

Category: Market Trends & Lead Times | Author: Klaus·Fischer | Published: May 2026 | Last Updated: May 15, 2026

Key Takeaways:

- Three simultaneous DDR4 EOL events — Samsung K4A8G085WC-BCTD, Micron MT53D1024M32D4DT-046 AAT:D, and Renesas 4RCD0229KB1ATG8 — are compressing the industrial procurement window to fewer than 18 months

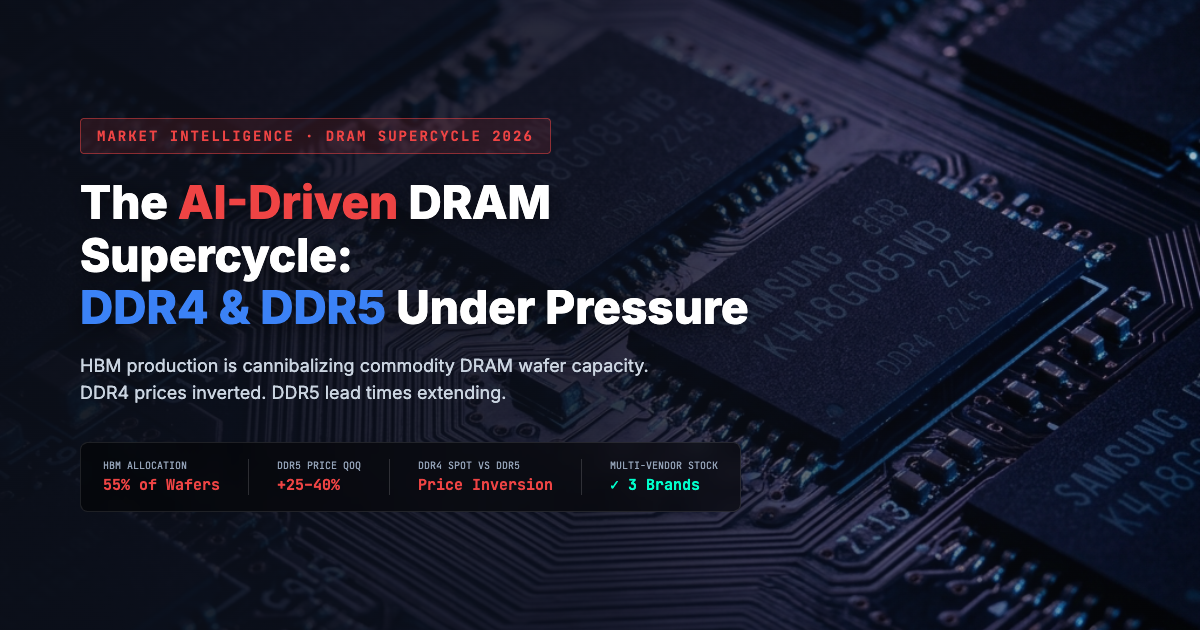

- HBM production for AI accelerators consumes 2.5–3× more wafer capacity per GB than conventional DDR4, structurally constraining legacy memory supply through at least late next year

- DDR4 contract prices have surged 30–50% quarter-over-quarter since mid-last year, with industrial-grade modules now trading at prices comparable to DDR5 equivalents

- Micron's LPDDR4X replacement MT53E1G32D2FW-046 AAT:C is NOT a drop-in swap — BSP, U-Boot, and Linux kernel DTS modifications are mandatory

- Samsung's K4A8G085WC-BIWE remains the last active suffix — but remaining production is locked under NCNR contracts for server-grade clients

- 📧 Submit an RFQ for DDR4 inventory → — icallin maintains verified DDR4 buffer stock across multiple densities for immediate shipment

1. Introduction — The Twilight of DDR4

For more than a decade, DDR4 SDRAM has served as the foundational memory architecture powering everything from enterprise servers and industrial PLCs to automotive infotainment systems and IoT gateways. Ratified by JEDEC in September 2012 and commercially deployed by 2014, DDR4 achieved something rare in the semiconductor industry: near-universal adoption across virtually every computing segment simultaneously.

That era is now ending — not gradually, but through a rapid convergence of three distinct end-of-life (EOL) events that are compressing the procurement window for industrial memory buyers with unprecedented speed.

Samsung Semiconductor has initiated its DDR4 phase-out program, transitioning flagship densities including the widely deployed K4A8G085WC series to Not Recommended for New Designs (NRND) status. Micron Technology has officially obsoleted its MT53D1024M32D4DT LPDDR4 product line, forcing embedded system designers into a non-trivial LPDDR4X migration that requires firmware-level validation. And Renesas Electronics has discontinued its 4RCD0229KB1ATG8 DDR4 Register Clock Driver — a component so deeply embedded in server RDIMM module production that most procurement teams do not even track it until supply vanishes.

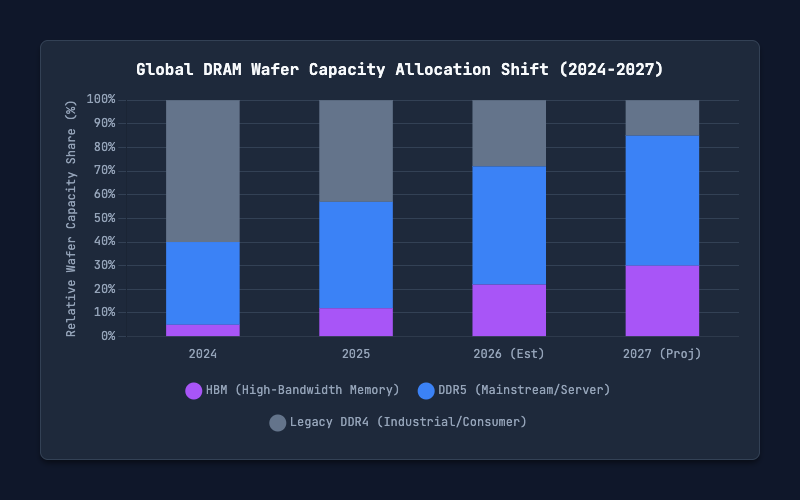

These three events are not coincidental. They share a common root cause: the explosive demand for High-Bandwidth Memory (HBM) driven by artificial intelligence infrastructure is consuming wafer capacity at a rate that makes legacy DDR4 production economically unsustainable for major manufacturers. Understanding this structural dynamic — and acting on it before the procurement window closes — is the central imperative for every industrial buyer reading this analysis.

2. The HBM Gravity Well — Why Wafer Capacity Is Disappearing

The most important number in semiconductor memory economics today is not a clock speed, a density figure, or a pricing forecast. It is a ratio: 2.5 to 3.0×. That is the multiple of raw silicon wafer area required to produce one gigabyte of HBM compared to one gigabyte of conventional DDR4 or DDR5.

This ratio exists because HBM is not simply "faster DRAM." It is an entirely different packaging architecture. Each HBM stack consists of multiple DRAM die layers (currently 8 to 12 in HBM3E configurations) bonded vertically using Through-Silicon Vias (TSVs) and micro-bump interconnects. Each individual die in the stack must pass stringent Known Good Die (KGD) testing before assembly, and the cumulative yield loss across multiple stacked layers means that manufacturers must start with significantly more raw silicon to achieve the same usable output.

The financial incentive structure amplifies this capacity reallocation. HBM commands average selling prices (ASPs) that are 5–8× higher per gigabyte than commodity DDR4. When Samsung, SK Hynix, and Micron evaluate how to allocate their finite wafer starts across product lines, the economic calculus overwhelmingly favors HBM production for AI accelerator customers who are signing multi-year, take-or-pay contracts worth billions of dollars.

Table 1: Wafer Capacity Consumption — HBM vs DDR4 vs DDR5 Comparison

| Parameter | DDR4 (Monolithic) | DDR5 (Monolithic) | HBM3E (8-Hi Stack) |

|---|---|---|---|

| Die per wafer (8Gb equiv.) | ~800–1,000 | ~600–800 | ~150–200 (per layer) |

| Layers per package | 1 | 1 | 8–12 |

| Effective wafer area per GB | 1.0× (baseline) | ~1.2× | 2.5–3.0× |

| Yield (typical) | 90–95% | 85–92% | 60–75% (stacked) |

| ASP per GB (contract) | $2.50–$4.00 | $3.50–$5.50 | $15–$25 |

| Primary demand driver | Legacy/Industrial | Mainstream/Server | AI Accelerators |

Table 1: Wafer capacity and economic comparison across DRAM architectures | Source: TrendForce, industry estimates | Compiled by: icallin.com

The consequence for DDR4 is structural and irreversible. Every wafer start redirected to HBM is a wafer start that does not produce DDR4. And because HBM demand is projected to grow at 50–60% CAGR through the end of the decade — driven by continued AI infrastructure buildout from hyperscalers including NVIDIA, AMD, Google, and Microsoft — the pressure on legacy memory supply will only intensify.

This is not a cyclical downturn that will self-correct. It is a permanent reallocation of manufacturing resources toward the highest-margin products. Industrial buyers who are planning their DDR4 procurement strategy around the assumption that "supply will normalize eventually" are operating on fundamentally flawed logic.

3. Samsung's DDR4 Phase-Out Timeline — K4A8G085WC Series Under the Microscope

Samsung's 8Gb DDR4 SDRAM product family — the K4A8G085WC series — has been one of the most widely deployed memory components in industrial computing. Used across everything from single-board computers and network switches to medical imaging systems and industrial automation controllers, this product family represents a massive installed base that is now facing a controlled but accelerating wind-down.

The K4A8G085WC-BCTD, one of the most popular suffixes in the series, has been transitioned to NRND status. Samsung has not issued a single dramatic "end of production" announcement. Instead, the company has implemented what industry observers describe as a "slow EOL" strategy: gradually reducing wafer starts for DDR4 product lines while extending limited production runs under Non-Cancellable, Non-Returnable (NCNR) contract terms for strategic server-grade customers.

This approach creates a dangerous illusion for the broader market. Small and medium-volume industrial buyers may observe that K4A8G085WC parts are still occasionally available through distribution channels and conclude that the EOL risk is exaggerated. In reality, the remaining supply is increasingly concentrated in the hands of tier-one server OEMs who locked in multi-quarter allocation agreements months or even years in advance.

Table 2: Samsung K4A8G085WC DDR4 Suffix Comparison

| Parameter | K4A8G085WC-BCTD | K4A8G085WC-BIWE | K4A8G085WC-BCRC |

|---|---|---|---|

| Density | 8Gb (1G × 8) | 8Gb (1G × 8) | 8Gb (1G × 8) |

| Speed grade | DDR4-2666 | DDR4-3200 | DDR4-2400 |

| tCK (min) | 0.75 ns | 0.625 ns | 0.833 ns |

| CAS Latency | CL19 | CL22 | CL17 |

| Operating voltage | 1.2V | 1.2V | 1.2V |

| Package | FBGA 78-ball | FBGA 78-ball | FBGA 78-ball |

| Temp. range | 0°C to +85°C | 0°C to +85°C | 0°C to +85°C |

| Production status | 🔴 NRND / EOL | 🟡 Active (limited) | 🔴 NRND / EOL |

| Migration note | Migrate to BIWE | Last active suffix | Migrate to BIWE |

Table 2: Samsung K4A8G085WC DDR4 suffix lifecycle comparison | Source: Samsung product catalog, distributor PCN data | Compiled by: icallin.com

The K4A8G085WC-BIWE — the DDR4-3200 speed grade — remains the last active suffix in the series. However, procurement teams should not interpret "active" as "abundantly available." Samsung has signaled through distribution channels that BIWE production is operating at reduced wafer starts, with priority allocation flowing to NCNR contract holders. Spot market availability is volatile and subject to significant price premiums.

For hardware designers maintaining existing DDR4 platforms, the BIWE suffix offers a viable bridge solution. The FBGA 78-ball package is pin-compatible across all K4A8G085WC suffixes, and the higher DDR4-3200 speed grade is backward-compatible with controllers designed for DDR4-2666 or DDR4-2400 — the memory controller simply operates the BIWE die at the lower frequency specified in the SPD EEPROM.

However, engineers must validate timing parameters carefully. Key parameters including tRFC (Refresh Cycle Time), tFAW (Four Activate Window), and tRRD (Row-to-Row Delay) differ between speed grades. A DDR4-2666 controller operating a DDR4-3200 DRAM at DDR4-2666 speeds will use DDR4-2666 timing parameters, but the DRAM's internal refresh behavior is defined by its native density and architecture, not the operating speed grade. Timing margin analysis using tools such as Micron's DDR Detective or Synopsys DDR PHY verification suites is strongly recommended before production deployment.

4. Micron's LPDDR4-to-LPDDR4X Forced Migration

While Samsung's DDR4 phase-out primarily impacts standard DIMM-based server and industrial computing platforms, Micron's parallel obsolescence of the MT53D1024M32D4DT LPDDR4 product line is creating acute disruption in the embedded systems and IoT segments.

The MT53D1024M32D4DT-046 AAT:D is a 32Gb (4GB) LPDDR4 SDRAM in a 200-ball BGA package, widely adopted in automotive infotainment systems, industrial HMI panels, edge AI compute modules, and IoT gateways. Its combination of low power consumption (1.1V VDDQ), high bandwidth (4,266 MT/s), and extended temperature support made it a default choice for power-sensitive embedded designs.

Micron has designated the MT53E1G32D2FW-046 AAT:C LPDDR4X as the official recommended replacement. On paper, the migration appears straightforward: LPDDR4X is an evolutionary extension of LPDDR4, offering the same interface width and similar signaling topology. In practice, however, this is not a drop-in replacement, and procurement teams who order MT53E parts expecting seamless interchangeability will encounter significant integration challenges.

Table 3: Micron MT53D (LPDDR4) vs MT53E (LPDDR4X) Parameter Comparison

| Parameter | MT53D1024M32D4DT-046 (LPDDR4) | MT53E1G32D2FW-046 (LPDDR4X) |

|---|---|---|

| Generation | LPDDR4 | LPDDR4X |

| Density | 32Gb (4GB) | 32Gb (4GB) |

| Data rate | 4,266 MT/s | 4,266 MT/s |

| I/O voltage (VDDQ) | 1.1V | 0.6V |

| Core voltage (VDD1/VDD2) | 1.1V / 1.1V | 1.1V / 1.05V |

| Package | 200-ball BGA | 200-ball BGA |

| Ball map | JEDEC LPDDR4 | JEDEC LPDDR4X (partially different) |

| Temp. range | -40°C to +105°C | -40°C to +105°C |

| Status | 🔴 Obsolete | 🟢 Active |

Table 3: LPDDR4 vs LPDDR4X critical parameter comparison | Source: Micron datasheets | Compiled by: icallin.com

The critical difference is the I/O voltage reduction from 1.1V to 0.6V. This is not a minor parametric change — it fundamentally alters the signaling environment. Board-level power delivery networks designed to supply 1.1V VDDQ must be redesigned with different voltage regulator output settings, different decoupling capacitor values, and potentially different PCB layer stackups to maintain signal integrity at the lower voltage swing.

Beyond hardware, the firmware migration is equally demanding. Embedded Linux platforms using the MT53D typically have Board Support Package (BSP) configurations that explicitly define LPDDR4 timing parameters in U-Boot device tree source (DTS) files. Switching to LPDDR4X requires modifying the DRAM controller initialization sequence, updating the MR (Mode Register) write values for the new voltage domain, and re-running DRAM training algorithms to establish optimal read/write eye margins at the 0.6V VDDQ level.

For platforms built on silicon vendors such as TI (TDA4VM), NXP (i.MX 8M), or Qualcomm (QCS/QCM series), the BSP update process typically involves obtaining updated DDR PHY initialization code from the silicon vendor — a process that can take 4–8 weeks for validation and release, assuming the vendor has already qualified the specific LPDDR4X part number.

5. Renesas DDR4 RCD — The Hidden Supply Chain Chokepoint

Of the three EOL events analyzed in this report, the Renesas 4RCD0229KB1ATG8 discontinuation is arguably the most consequential for enterprise infrastructure — yet it receives the least attention from procurement teams.

A Register Clock Driver (RCD) is a specialized buffer IC that sits on every Registered DIMM (RDIMM) and Load-Reduced DIMM (LRDIMM) used in enterprise servers and data center platforms. The RCD re-drives the command, address, and control signals from the memory controller to the DRAM devices on the module, enabling the higher module densities (64GB, 128GB, 256GB per DIMM) that enterprise workloads demand.

The 4RCD0229KB1ATG8 is Renesas' DDR4-generation RCD — a component that is present on virtually every DDR4 RDIMM module shipped by module manufacturers including Samsung, SK Hynix, Micron, and Kingston. When this component goes out of production, it does not merely affect one OEM or one product line. It threatens the entire DDR4 RDIMM ecosystem.

Most procurement teams do not directly purchase RCD components. Instead, they purchase finished DIMM modules from memory module manufacturers. The RCD is a "hidden" component buried in the module's bill of materials. This means that the EOL impact is experienced indirectly — as extended lead times, reduced module availability, or unexpected price increases — without the root cause being immediately apparent to the end buyer.

The domestic alternative is the Montage Technology M88DDR4RCD02 — a functionally equivalent DDR4 RCD developed by Shanghai-based Montage Technology, a company that has steadily expanded its presence in the server memory buffer IC market. The M88DDR4RCD02 has been qualified by several major module manufacturers and is currently shipping in production volumes for the Chinese domestic server market.

Table 4: Renesas 4RCD0229KB1ATG8 vs Montage M88DDR4RCD02 Specification Comparison

| Parameter | Renesas 4RCD0229KB1ATG8 | Montage M88DDR4RCD02 |

|---|---|---|

| Function | DDR4 Register Clock Driver | DDR4 Register Clock Driver |

| JEDEC compliance | DDR4 RCD02 (JESD82-31A) | DDR4 RCD02 (JESD82-31A) |

| Max data rate | DDR4-3200 | DDR4-3200 |

| Input registers | 2 (A/B side) | 2 (A/B side) |

| Output drivers | 22 (CA) + 4 (CK) | 22 (CA) + 4 (CK) |

| Package | FBGA 144-ball | FBGA 144-ball |

| Operating voltage | 1.2V | 1.2V |

| Production status | 🔴 EOL | 🟢 Active |

| Qualification | Global OEM qualified | Domestic OEM qualified, expanding |

| Key consideration | — | Requires module-level revalidation |

Table 4: DDR4 RCD specification comparison — Renesas vs Montage domestic alternative | Source: Renesas/Montage datasheets | Compiled by: icallin.com

The M88DDR4RCD02 is pin-compatible and functionally compliant with the same JEDEC RCD02 specification. However, switching RCD suppliers on an existing RDIMM module design is not a simple component swap. Module manufacturers must re-run their entire validation suite — including signal integrity testing, thermal characterization, and platform-level compatibility testing across multiple server motherboard vendors (Intel Purley/Whitley, AMD Turin/Genoa) — before shipping modules with the new RCD to enterprise customers.

This qualification process typically takes 3–6 months, during which module manufacturers must maintain parallel production lines or build buffer inventory with the legacy Renesas RCD. For procurement teams purchasing finished RDIMM modules, the practical implication is that DDR4 RDIMM availability will be constrained during this transition period, with premium pricing for modules that have already been qualified with the Montage replacement.

6. DDR4 Price Trajectory and Lead Time Forecast Through 2027

The pricing environment for DDR4 SDRAM has undergone a paradigm shift that fundamentally breaks the historical cyclical model. In previous memory market cycles, periods of high pricing were followed by capacity expansion, oversupply, and price corrections — a pattern that repeated roughly every 3–4 years. This cycle has been disrupted by the structural reallocation of manufacturing capacity toward HBM and advanced DDR5 products.

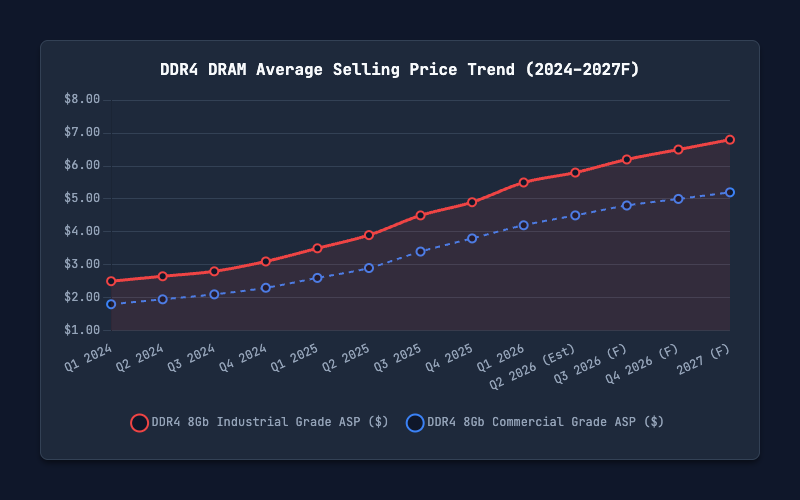

DDR4 contract prices began their sustained upward trajectory in mid-2025, driven by the initial wave of EOL announcements and the growing recognition that new DDR4 wafer capacity would not be built. By early this year, DDR4 8Gb components that had traded at approximately $2.50 per unit in early 2024 were commanding $4.00–$5.50 in contract pricing — a 60–120% increase over an 18-month period.

More concerning for industrial buyers is the convergence phenomenon: DDR4 pricing is now approaching — and in some spot market transactions exceeding — DDR5 equivalent pricing. This price inversion, where the older technology costs as much as or more than its successor, is a clear market signal that DDR4 supply is entering a terminal scarcity phase.

Table 5: DDR4 Lead Time Comparison Across Top Global Distributors (Q2 2026)

| Distributor | DDR4 8Gb (Commercial) | DDR4 8Gb (Industrial) | DDR4 RDIMM 32GB | DDR4 LPDDR4 4GB |

|---|---|---|---|---|

| Distributor A (Tier 1) | 14–18 weeks | 20–26 weeks | 16–22 weeks | EOL — No stock |

| Distributor B (Tier 1) | 12–16 weeks | 18–24 weeks | 14–20 weeks | Limited (LTB only) |

| Distributor C (Regional) | 8–12 weeks | 14–20 weeks | Allocation only | EOL — No stock |

| Distributor D (Independent) | 4–8 weeks | 8–14 weeks | 6–10 weeks | Spot only |

| icallin.com | Immediate | 2–4 weeks | Available | Buffer stock |

Table 5: DDR4 lead time comparison across distribution channels, Q2 2026 | Source: Distributor surveys, icallin supply chain data | Compiled by: icallin.com

The data reveals a striking pattern: industrial-grade DDR4 components consistently carry lead times that are 40–60% longer than commercial-grade equivalents. This premium reflects the smaller production volumes, stricter testing requirements (extended temperature validation, enhanced reliability screening), and the fact that industrial-grade memory is typically produced on older, more mature process nodes that are the first to be retired when manufacturers reallocate capacity.

Independent distributors with verified buffer inventory — such as icallin — have emerged as a critical supply chain resource for buyers who cannot wait 20+ weeks for factory allocation. The ability to ship from warehouse stock within days rather than months represents a meaningful competitive advantage for production lines that face imminent supply disruption.

Looking ahead, the consensus among industry analysts including TrendForce, Gartner, and IDC is that meaningful DDR4 price relief is not expected before late next year at the earliest. The combination of continued HBM capacity absorption, accelerating DDR4 EOL programs, and limited new wafer capacity coming online creates a supply environment where DDR4 pricing will remain at elevated levels — and potentially continue rising — through the end of this year and well into next year.

For procurement teams, the strategic implication is clear: planning budgets based on historical DDR4 pricing is no longer viable. BOM cost models must be updated to reflect the new reality of structurally higher memory pricing, and alternative sourcing strategies must be activated immediately.

7. Strategic Procurement Playbook — Five Actions to Take Before Q4 2026

Based on the analysis presented in this report, we recommend the following five-point action plan for industrial procurement teams managing DDR4-dependent production lines:

Action 1: Execute Last-Time Buy (LTB) for Critical DDR4 SKUs Immediately

For every DDR4 component on your active BOM that has received an NRND or EOL notification, calculate your remaining production lifetime demand and place LTB orders now. Do not wait for the formal Last-Time Buy deadline — by the time the official cutoff arrives, available inventory will be severely depleted and pricing will reflect scarcity premiums. Prioritize industrial-grade and extended-temperature components, which are the first to disappear from the market.

Action 2: Qualify DDR4-to-DDR5 Bridge Designs for Next-Generation Platforms

Begin the DDR5 qualification process for your next product generation immediately. Even if your current platform cannot accommodate DDR5 (due to controller limitations or PCB constraints), starting the design validation pipeline now ensures that your next-generation product will not inherit the same DDR4 dependency. Target DDR5-4800 as the initial migration speed grade, as it offers the broadest controller compatibility.

Action 3: Diversify Supplier Base Including Domestic Alternatives

The Renesas RCD EOL has demonstrated the vulnerability of single-source dependency in the memory supply chain. Evaluate domestic alternatives such as Montage Technology for DDR4 buffer ICs, and consider secondary DRAM sources including Nanya Technology and CXMT for standard DDR4 densities where design flexibility permits.

Action 4: Lock Multi-Quarter Allocation Agreements with NCNR Terms

For DDR4 components that must remain in production for more than 12 months, negotiate multi-quarter allocation agreements with your primary distributors. Accept NCNR (Non-Cancellable, Non-Returnable) terms if necessary — the cost of carrying excess DDR4 inventory is far lower than the cost of a production line shutdown due to memory unavailability.

Action 5: Partner with Verified Independent Distributors for Buffer Inventory

Authorized distribution channels are increasingly unable to guarantee DDR4 availability within commercially acceptable lead times. Independent distributors with AS6081/AS6171-verified inventory management systems provide a critical buffer layer for time-sensitive procurement requirements. Verify traceability documentation, request batch-level testing reports, and confirm that components are sourced from authorized supply chains.

Table 6: DDR4 EOL Risk Assessment Matrix by Application Segment

| Application Segment | EOL Risk Level | Primary Exposure | Recommended Action | Timeline |

|---|---|---|---|---|

| Enterprise Servers (RDIMM) | 🔴 Critical | RCD EOL + DRAM EOL | LTB + Montage qualification | Immediate |

| Industrial Automation (UDIMM) | 🔴 Critical | Samsung 8Gb EOL | LTB + DDR5 bridge design | Q3 this year |

| Automotive Infotainment | 🟡 High | LPDDR4 obsolescence | LPDDR4X migration + BSP update | Q3–Q4 this year |

| IoT Gateways / Edge | 🟡 High | LPDDR4 obsolescence | LPDDR4X migration or DDR5 skip | Q4 this year |

| Networking / Telecom | 🟡 High | DDR4 RDIMM shortage | Multi-source qualification | Q3 this year |

| Consumer Electronics | 🟢 Moderate | DDR5 transition underway | Natural migration cycle | Next year |

Table 6: DDR4 EOL risk assessment by application segment | Source: icallin market intelligence | Compiled by: icallin.com

Frequently Asked Questions

Q1: When will Samsung completely stop producing DDR4 SDRAM?

Samsung has not announced a single definitive "last production date" for its entire DDR4 product line. Instead, the company is implementing a phased wind-down approach. Specific suffixes such as the K4A8G085WC-BCTD have already entered NRND status, while others like the K4A8G085WC-BIWE remain in limited production under NCNR contract terms. Based on current trajectory analysis, industry analysts expect Samsung to substantially exit DDR4 production by late next year to early the year after, with only residual volumes maintained for long-lifecycle industrial and automotive customers under specific contractual obligations.

Q2: Is the Micron MT53E1G32D2FW a direct drop-in replacement for the MT53D1024M32D4DT?

No. While both components share the same 32Gb density and 200-ball BGA package form factor, the MT53E1G32D2FW (LPDDR4X) operates at a fundamentally different I/O voltage of 0.6V compared to the MT53D's 1.1V VDDQ. This voltage difference requires PCB power delivery network modifications, updated voltage regulator configurations, and comprehensive firmware changes including U-Boot device tree source (DTS) updates and DRAM controller initialization sequence modifications. Silicon vendor BSP updates are typically required and can take 4–8 weeks to validate. Full board-level signal integrity analysis should be performed before production deployment.

Q3: How does HBM production affect DDR4 pricing for industrial buyers?

HBM production directly reduces DDR4 supply by competing for the same semiconductor wafer capacity. Producing one gigabyte of HBM requires approximately 2.5–3× more raw silicon wafer area than one gigabyte of conventional DDR4. As manufacturers prioritize HBM production for high-margin AI accelerator contracts, the wafer starts available for DDR4 are structurally reduced. This supply constraint has driven DDR4 contract prices up by 30–50% quarter-over-quarter since mid-last year, with industrial-grade components experiencing even steeper increases due to their smaller production volumes and stricter testing requirements.

Q4: What is a DDR4 RCD and why does its EOL matter for server procurement?

A Register Clock Driver (RCD) is a buffer IC present on every DDR4 Registered DIMM (RDIMM) and Load-Reduced DIMM (LRDIMM) used in enterprise servers. The RCD re-drives command, address, and control signals from the memory controller to the DRAM devices, enabling the high-density configurations (64GB–256GB per DIMM) that enterprise workloads require. The Renesas 4RCD0229KB1ATG8 is the dominant DDR4-generation RCD. Its discontinuation threatens the entire DDR4 RDIMM module supply chain, as module manufacturers cannot build RDIMMs without this component. The domestic alternative — Montage Technology M88DDR4RCD02 — requires 3–6 months of module-level revalidation before production deployment.

Q5: Should we switch to DDR5 now or stockpile DDR4 for legacy platforms?

The answer depends on your product lifecycle timeline. For platforms with remaining production lifetimes of less than 18 months, executing a Last-Time Buy for DDR4 inventory is more cost-effective and lower-risk than redesigning for DDR5. For platforms with production horizons extending beyond next year, investing in a DDR5 migration design is strategically essential — DDR4 supply will become increasingly difficult and expensive to source beyond that timeframe. Many organizations are pursuing a dual strategy: stockpiling DDR4 for current-generation platforms while simultaneously qualifying DDR5 for next-generation designs.

Q6: How can independent distributors like icallin help mitigate DDR4 supply risks?

Independent distributors with verified inventory management systems provide a critical supply chain buffer when authorized distribution channels cannot meet lead time requirements. icallin maintains DDR4 buffer stock across multiple densities and configurations, available for immediate shipment with full traceability documentation. Unlike authorized distributors who are constrained by factory allocation schedules, independent distributors can source from multiple authorized supply chains, identify available inventory across global markets, and provide rapid turnaround for time-sensitive production requirements. All components are verified through AS6081/AS6171-compliant processes to ensure authenticity and reliability.

Conclusion: The Window Is Closing — Act Now

The DDR4 sunset is not a distant forecast — it is an active, accelerating process driven by forces that are structural and irreversible. The convergence of Samsung's K4A8G085WC phase-out, Micron's LPDDR4 obsolescence, and Renesas' DDR4 RCD discontinuation creates a three-front procurement pressure that no single mitigation strategy can address in isolation.

The HBM gravity well — consuming 2.5–3× more wafer capacity per gigabyte while commanding 5–8× higher margins — ensures that legacy DDR4 production will continue to shrink as manufacturers chase AI infrastructure revenue. DDR4 pricing has already broken free from historical cyclical patterns and is now on a structurally elevated trajectory that will persist through at least late next year.

For industrial procurement teams, the message is unambiguous: the window to secure DDR4 supply at commercially viable pricing and lead times is measured in months, not years. Execute Last-Time Buys for critical SKUs. Begin DDR5 qualification for next-generation platforms. Diversify your supplier base. Lock in allocation agreements. And partner with verified independent distributors who can bridge the gap between factory lead times and production line requirements.

The organizations that act decisively now will navigate this transition with minimal disruption. The organizations that wait will find themselves competing for increasingly scarce supply at increasingly unfavorable terms.

📧 Submit an RFQ for DDR4 Memory Components →

Related Internal Resources

- Samsung K4A8G085WC-BCTD — Product Detail

- Samsung Manufacturer Page

- Memory IC Category

- Submit RFQ

- Hot Products

*Rebecca·Cohen is a Senior Market Analyst at icallin.com, specializing in memory semiconductor pricing, lead time forecasting, and supply chain dynamics. With extensive experience tracking DRAM and Flash inventory cycles, Rebecca provides actionable market intelligence for industrial procurement teams.

Top Recommended part