XC7K325T-2FFG900I Availability 2026 | Kintex-7 FPGA Supply

XC7K325T-2FFG900I Availability 2026: Why Kintex-7 FPGA Supply Is Still Tight

Category: Market Trends & Lead Times | Author: Charles·Lee | Published: March 2026 | Last Updated: March 21, 2026

Key Takeaways:

- XC7K325T-2FFG900I factory lead times remain at 22–31 weeks as of March 2026

- Authorized distributors hold near-zero buffer stock (1–2 units at Mouser/DigiKey)

- TSMC's 28nm foundry capacity reallocation is a structural, not cyclical, constraint

- AMD supports Kintex-7 through 2040 but will not expand production capacity

- Recommended actions: 6–12 month forecast horizons and 2–4 months of safety stock

- New designs should evaluate Kintex UltraScale+ to escape the 28nm capacity bottleneck

If you've been tracking Kintex-7 FPGA lead times since the 2021–2023 semiconductor supercycle, you might have expected the situation to normalize by now. After all, headline chip shortage stories have largely faded from mainstream media, and many semiconductor categories have returned to healthy inventory levels.

But heading into Q2 2026, procurement teams sourcing high-performance FPGAs are encountering a frustrating and persistent reality. Availability for the XC7K325T-2FFG900I — one of the most widely designed-in Kintex-7 variants — remains uneven. Pricing is elevated compared to pre-shortage baselines. And factory lead times continue to stretch well beyond what "normal" used to mean.

This isn't just a minor inconvenience. For companies with the XC7K325T deeply embedded in production BOMs across telecom, defense, medical imaging, and industrial automation programs, supply unpredictability creates cascading risks: missed delivery commitments, emergency spot-market buys at premium prices, and — in worst cases — production line shutdowns that burn through project margins overnight.

So what's actually happening with Kintex-7 supply? Why hasn't it recovered in line with broader semiconductor normalization? And what should hardware teams, supply chain managers, and procurement directors take away from the current XC7K325T-2FFG900I market picture when building their 2026 FPGA strategies?

Let's break it down with data, context, and actionable recommendations.

XC7K325T-2FFG900I Technical Specifications and Key Applications

Before diving into supply dynamics, it's worth understanding why the XC7K325T-2FFG900I commands such attention in the FPGA procurement world. This isn't just any commodity chip — it's a mid-to-high-density programmable logic device that sits at a critical performance-cost intersection.

Full Technical Profile

The XC7K325T-2FFG900I is a member of AMD's (formerly Xilinx) Kintex-7 FPGA family, fabricated on TSMC's 28nm HPL (High-Performance, Low-Power) process. Here are its core specifications:

| Parameter | Value |

|---|---|

| Logic Cells | 326,080 |

| CLB Slices | 25,475 |

| DSP48E1 Slices | 840 |

| Block RAM | 16,020 Kb |

| Distributed RAM | 1,188 Kb |

| User I/Os | 500 (FFG900 package) |

| GTX Transceivers | 16 (up to 12.5 Gb/s per lane) |

| PCIe Support | Gen1/Gen2, up to 8 lanes |

| XADC | Dual 12-bit, 1 MSPS ADCs |

| Package | FFG900 BGA (31 × 31 mm) |

| Speed Grade | -2 (balanced performance/power) |

| Core Voltage | 1.0V |

| I/O Voltage | 1.8V / 2.5V / 3.3V |

| Temperature Range | Industrial: –40 °C to +100 °C (Tj) |

| Process Node | 28nm HKMG |

Where the XC7K325T-2FFG900I Is Designed In

The XC7K325T-2FFG900I has been adopted across an impressively broad range of applications, which is precisely what makes supply pressures so impactful:

-

Telecommunications Infrastructure — 4G/LTE base stations, 5G radio units, distributed baseband architectures, and packet processing engines. The combination of high-speed transceivers and substantial DSP resources makes it a natural fit for fronthaul and midhaul signal processing.

-

Defense & Aerospace — Radar signal processing, electronic warfare systems, secure communications, and software-defined radio (SDR) platforms. The industrial temperature rating and long-lifecycle commitment from AMD make it attractive for programs with 15–20 year operational lifespans.

-

Medical Imaging — Portable ultrasound equipment, CT scanner data acquisition, and MRI signal processing chains. The parallel processing capability of 840 DSP slices enables real-time image reconstruction that discrete DSP solutions struggle to match.

-

Industrial Automation — Machine vision, motor drive control, high-speed data acquisition systems, and programmable logic controllers (PLCs). The FPGA's reconfigurability allows field updates without hardware changes.

-

Video-over-IP & Broadcast — Single-chip implementations for video gateways, 4K/8K video encoding assist, and low-latency streaming infrastructure.

-

Test & Measurement — Custom triggering systems, hardware-timed test sequencers, and protocol-aware digital testing platforms (notably used in National Instruments/NI FlexRIO modules).

-

Energy & Power Systems — Grid-tied inverter control, battery management systems (BMS), and MPPT controllers for solar installations.

The critical insight here is that once the XC7K325T is designed into a product — which often takes 12–18 months of development — customers are essentially locked in. The cost and risk of migrating to a different FPGA (even within the same family) typically outweighs paying premium spot-market prices for a constrained part.

XC7K325T-2FFG900I Stock Levels and Lead Times — March 2026 Data

Let's put concrete numbers on the table. Here's a channel-by-channel breakdown of XC7K325T-2FFG900I availability as of mid-March 2026, compiled from publicly listed distributor data:

Authorized Distributor Stock Availability

| Distributor | Region | Stock (units) | Factory Lead Time | Notes |

|---|---|---|---|---|

| Mouser | Global | 1–2 | 31 weeks | Minimal buffer; bulk orders face allocation |

| Mouser | Europe | 1 | 22 weeks | Slightly better lead time for EU allocation |

| DigiKey | Global | 2 | 22 weeks (MSLT) | Spot qty available; production volumes require scheduling |

| Farnell | Israel/EMEA | Available to order | 24 weeks | Manufacturer standard lead time |

| LCSC | Asia-Pacific | 1,000+ | Immediate | Likely Asia-channel sourced; verify date codes |

| Nantian Electronics | China | Substantial inventory | 1–2 business days | Independent; quality verification recommended |

What This Stock Data Tells Us

Authorized channels are running near-zero buffer stock. Mouser and DigiKey each hold 1–2 units — essentially sample quantities. This means any production-volume order (50+ units) will be subject to factory lead times.

Factory lead times remain 22–31 weeks. Depending on region and allocation, you're looking at 5.5 to 8 months from order to delivery. Pre-shortage, typical lead times for Kintex-7 FPGAs were 12–16 weeks.

Asia-Pacific channels show higher apparent availability. LCSC lists 1,000+ units in stock. While this is encouraging, procurement teams should exercise due diligence: verify date codes, check for potential remarked or recycled parts, and consider using AS6081/AS6171-certified inspection before accepting delivery.

Pricing is elevated. While we won't quote specific prices (they change daily), market data suggests current authorized pricing for the XC7K325T-2FFG900I is 30–50% above 2019 baseline levels, and spot-market pricing from independents can run 2–3x authorized pricing for immediate-ship quantities.

How XC7K325T Compares to Other Kintex-7 Variants

To put the XC7K325T supply situation in context, here's how lead times compare across the Kintex-7 family:

| Device | Logic Cells | Typical Lead Time (Mar 2026) | Relative Availability |

|---|---|---|---|

| XC7K70T | 65,600 | 16–20 weeks | ✅ Better — lower demand, smaller die |

| XC7K160T | 162,240 | 20–28 weeks | ⚠️ Moderate — popular in mid-range apps |

| XC7K325T | 326,080 | 22–31 weeks | 🔴 Tight — highest demand variant |

| XC7K355T | 356,160 | 24–32 weeks | 🔴 Tight — similar die, lower volume |

| XC7K410T | 406,720 | 26–35 weeks | 🔴 Very tight — largest die, lowest yield |

| XC7K480T | 477,760 | 28–40 weeks | 🔴 Extremely tight — limited production |

The pattern is clear: larger die sizes correlate with longer lead times, because they yield fewer good devices per wafer. The XC7K325T sits in the unfortunate sweet spot of being large enough to be yield-constrained, while also being the most popular variant in terms of design-in volume.

Kintex-7 vs Artix-7 vs Virtex-7: Why Engineers Can't Simply Switch

Understanding the competitive landscape within AMD's own product line helps explain why the Kintex-7 occupies such a unique and difficult-to-replace position.

AMD 7-Series FPGA Family Comparison Table

| Parameter | Artix-7 | Kintex-7 | Virtex-7 |

|---|---|---|---|

| Positioning | Cost-optimized, low power | Performance/watt sweet spot | Maximum performance |

| Max Logic Cells | 215,360 | 477,760 | 1,955,000 |

| Max DSP Slices | 740 | 1,920 | 3,600 |

| Max Block RAM (Kb) | 13,140 | 34,380 | 67,680 |

| Transceiver Speed | Up to 6.6 Gb/s | Up to 12.5 Gb/s (GTX) | Up to 28.05 Gb/s (GTH) |

| Peak DSP Performance | 930 GMACs | 2,845 GMACs | 5,335 GMACs |

| Peak I/O Bandwidth | 211 Gb/s | ~800 Gb/s | 2,784 Gb/s |

| DDR3 Support | Up to 1,066 Mb/s | Up to 1,866 Mb/s | Up to 1,866 Mb/s |

| Target Applications | IoT, portable medical, cost-sensitive | Telecom, defense, signal processing | HPC, 100G networking, ASIC prototyping |

| Typical Unit Price | $15–$150 | $100–$800 | $500–$5,000+ |

| Supply Status (Mar 2026) | Generally available | ⚠️ Constrained | 🔴 Very constrained |

| Power Efficiency | Best per logic cell | Best performance/watt | Highest absolute perf |

Why Switching FPGA Families Is Not a Quick Fix

A common question from non-technical procurement managers is: "If Kintex-7 is tight, why not just use Artix-7 or move to UltraScale?"

The reality is more complicated:

Artix-7 lacks the transceiver performance. Artix-7's 6.6 Gb/s GTP transceivers can't replace Kintex-7's 12.5 Gb/s GTX transceivers in telecom and high-speed applications. For many designs, the transceiver is the bottleneck, not the logic.

Virtex-7 is even more constrained (and expensive). Moving "up" to Virtex-7 would solve the performance question but at 5–10× the cost and with even worse lead times.

UltraScale/UltraScale+ migration requires re-design. While AMD offers migration guides, moving from 7-Series to UltraScale involves changes to pin assignments, power supply design, timing constraints, and IP core compatibility. This typically represents a 6–12 month engineering effort with associated re-qualification costs of $50K–$500K+ depending on regulatory requirements (particularly in defense and medical).

Intel/Altera alternatives require a full platform change. Switching from Xilinx to Intel FPGA tools (Quartus vs. Vivado), IP ecosystems, and board-level design is even more disruptive — effectively a complete product redesign.

This lock-in effect is why Kintex-7 supply tightness has such outsized commercial impact. Engineers and procurement teams don't have easy escape valves.

Why Kintex-7 FPGA Lead Times Remain at 22–31 Weeks in 2026

Several interconnected factors are keeping Kintex-7 availability tighter than the broader semiconductor market recovery would suggest. Understanding these drivers is essential for building realistic procurement forecasts.

28nm Foundry Capacity Is Being Actively Reallocated by TSMC

The Kintex-7 family is manufactured on TSMC's 28nm node — a mature process that is undergoing a structural shift in capacity allocation.

According to TrendForce and Counterpoint Research reports from late 2025 and early 2026:

-

TSMC is actively reducing its direct mature-node output to reallocate capacity toward advanced processes (3nm, 2nm) and advanced packaging (CoWoS, SoIC), where profit margins are significantly higher.

-

TSMC plans to reduce 12-inch mature-node capacity at Fab14 by 15–20% by 2028, transferring some equipment to Vanguard International Semiconductor (VIS) in Singapore.

-

TSMC's expansion priorities are overwhelmingly focused on leading-edge nodes: 3nm monthly capacity is projected to hit 180,000–200,000 wafers by end of 2026, while 2nm capacity targets 95,000–100,000 wafers per month.

What this means for Kintex-7: AMD/Xilinx must compete for a shrinking pool of 28nm wafer starts alongside dozens of other fabless companies producing automotive MCUs, IoT SoCs, industrial ICs, RF transceivers, and power management devices.

The 28nm node serves over 80% of chips used in 5G base stations and automotive electronics — creating intense allocation pressure.

Chart summary: Automotive MCUs & SoCs represent the largest share (~25%) of 28nm wafer demand in 2026, followed by Industrial & IoT (~20%) and Telecom & 5G (~18%). FPGAs account for roughly 12% of total 28nm demand, creating intense competition for wafer allocation.

FPGA Demand Has Structurally Shifted — Not Declined

The post-pandemic FPGA demand surge didn't evaporate; it transformed into sustained, structurally higher baseline demand driven by multiple reinforcing trends:

| Demand Driver | Impact on Kintex-7 | Growth Trajectory |

|---|---|---|

| 5G Infrastructure | Direct — baseband processing, beamforming | Expanding into emerging markets |

| AI Edge Inference | Growing — FPGAs as flexible accelerators | Accelerating as models shrink |

| Defense Modernization | Strong — radar, EW, secure comms | Multi-year funded programs |

| Energy Transition | Emerging — inverter control, BMS, grid storage | Policy-driven global expansion |

| Medical Device Growth | Steady — imaging, diagnostics, portable devices | Post-COVID investment boom |

| Industrial Automation | Steady — machine vision, robotics, PLCs | Industry 4.0 adoption wave |

| Satellite & Space | New — LEO constellation processing | Rapid deployment phase |

The global FPGA market is projected to reach $10–$14 billion in 2025 and $11–$15 billion in 2026, depending on the research source — representing compound annual growth rates of 8–12%. AMD/Xilinx, Intel/Altera, and Achronix collectively hold over 70% of the high-end FPGA market, with AMD commanding the largest share.

AMD's Portfolio Strategy Deprioritizes 7-Series Capacity Expansion

AMD has officially extended the lifecycle of all 7-Series FPGAs through at least 2035, with some devices supported until 2040. This is excellent news for design longevity — your XC7K325T-based product won't face an abrupt end-of-life cliff.

However, this support commitment is fundamentally a maintenance strategy, not a growth strategy. AMD's investment priorities are clearly focused on:

- Versal Adaptive SoC — the current flagship adaptive computing platform

- Kintex UltraScale+ Gen 2 — announced February 2026, mass production expected H1 2027, supported through 2045

- AI-optimized compute products — competing with NVIDIA in the data center acceleration space

AMD has no commercial incentive to negotiate additional 28nm wafer capacity for a product family that generates lower per-unit revenue than their advanced-node products. The 7-Series will be sustained but not expanded — meaning supply will remain structurally constrained at whatever production level AMD has currently contracted with TSMC.

Geopolitical Tensions Add Allocation Uncertainty

The semiconductor industry operates in an increasingly complex geopolitical environment:

-

US-China trade restrictions continue to create allocation uncertainties, particularly for dual-use technologies like high-performance FPGAs.

-

Export control regulations require additional compliance overhead for distributors and end-users.

-

Regional supply chain diversification efforts (US CHIPS Act, EU Chips Act, Japan's semiconductor subsidies) are reshaping global manufacturing geography, but primarily for advanced nodes — mature 28nm capacity is not a focus area for government investment.

For Kintex-7 procurement specifically, these dynamics can create allocation imbalances where certain regions receive disproportionate supply while others face extended wait times.

What FPGA Engineers Say About Kintex-7 Shortage on Reddit and Industry Forums

Beyond official market data, it's instructive to look at what engineers and procurement professionals are actually experiencing on the ground. Here are recurring themes from technical forums and industry communities:

Real Feedback from Reddit's r/FPGA Community

Engineers on Reddit have documented the progression of Kintex-7 availability challenges since the semiconductor crisis began:

"The 7K325 used to be a $200 part that you could get in a week. During the Great Shortage, we saw quotes at $1,200+ with 52-week lead times. Prices have come down, but we're still paying 40% more than 2019, and lead times are 5–6 months minimum."

"We tried to second-source with Altera [Intel] but the engineering cost to requalify our design exceeded the BOM savings over three years. So we're stuck on Kintex-7 and just carrying more inventory."

"If you're starting a new design today, UltraScale+ is the right choice. But if you're mid-production, you have no good alternatives. You either commit to 6–12 months of buffer stock or accept schedule risk."

Findings from Industry Surveys and Reports

-

Fusion Worldwide (a major independent distributor) reports that "lead times for high-performance Xilinx devices, particularly automotive-qualified Kintex-7 parts like the XC7K160T-2FFG676I, have exceeded 52 weeks" and that "the Xilinx supply chain is unlikely to fully stabilize until mid-2026."

-

Semiconductor procurement surveys indicate that FPGAs remain among the top 5 most difficult component categories to source in 2025–2026, alongside automotive MCUs, high-end power management ICs, certain memory types, and advanced analog/mixed-signal devices.

6 Procurement Strategies for Sourcing XC7K325T-2FFG900I in 2026

Based on the structural analysis above, here are concrete strategies we recommend for teams with XC7K325T-2FFG900I (or any Kintex-7 variant) on their BOMs:

Strategy 1: Extend Your Planning Horizon to 6–12 Months

Stop thinking in 8–12 week procurement cycles. For Kintex-7 FPGAs, you should be working with 6- to 12-month rolling demand forecasts and placing orders (or at least reserving allocation) well in advance. Share forecasts with your distributors — many authorized channels will honor allocation commitments backed by firm forecasts, even when stock is tight.

Strategy 2: Diversify Your Sourcing Channels

Relying solely on a single authorized distributor is risky in the current environment. A robust sourcing strategy should include:

| Source Type | Advantages | Risk Mitigation Required |

|---|---|---|

| Primary authorized distributor | Guaranteed authentic, warranty support | May have allocation limits |

| Secondary authorized distributor | Additional allocation pool | Requires separate account setup |

| Franchised independent distributor | Broader market access, cross-reference capabilities | Verify AS6081/AS6171 certification |

| Asia-Pacific spot market | Higher apparent availability, competitive pricing | Mandatory incoming inspection (X-ray, decap, date code verification) |

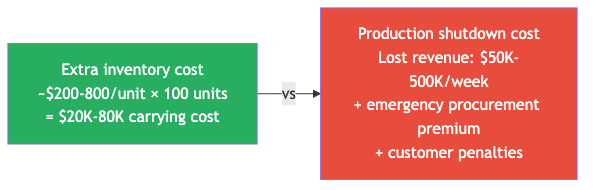

Strategy 3: Build and Maintain Safety Stock

For production-critical FPGAs, maintaining a safety stock of 2–4 months' supply is no longer overly cautious — it's baseline risk management. Calculate the cost of carrying extra inventory versus the cost of a production line shutdown:

Chart summary: Carrying 100 units of buffer stock costs $20K–$80K, while a single week of production shutdown can cost $50K–$500K in lost revenue, plus emergency procurement premiums and customer penalties. The math overwhelmingly favors buffer stock.

The math almost always favors carrying buffer stock for components with 20+ week lead times.

Strategy 4: Implement Incoming Quality Inspection

If you're sourcing from any non-authorized channel — or even receiving shipments from authorized distributors with unusual date codes — implement a quality inspection protocol:

- Visual inspection — magnification check of package markings, lead condition, and pin alignment

- X-ray inspection — verify internal die/wire bond structure against known-good references

- Electrical test — boundary scan (JTAG) verification; check for correct device ID, DNA, and functionality

- Date code verification — ensure consistency with expected manufacturing dates; reject units with suspiciously recent date codes on EOL packages

- Decap testing (for high-risk sourcing) — destructive testing of sample units to verify die marking matches package marking

Strategy 5: Evaluate the Kintex UltraScale+ Migration Path

While migrating your current production design is rarely practical, new designs starting in 2026 should strongly consider Kintex UltraScale+ (or the upcoming Gen 2 variant):

| Factor | Kintex-7 | Kintex UltraScale+ | KU+ Gen 2 (2027+) |

|---|---|---|---|

| Process Node | 28nm | 20nm | 16nm (expected) |

| Performance/Watt | Baseline | ~2× improvement | ~3× improvement |

| Transceiver Speed | 12.5 Gb/s | 16.3 Gb/s | TBD (expected higher) |

| Supply Outlook | Constrained through 2026+ | Improving | New production ramp |

| Lifecycle Support | Through 2035–2040 | Through 2040+ | Through 2045+ |

| Vivado Toolchain | Supported (maintenance mode) | Full support | Full support |

| Migration Effort | N/A | Moderate (6–12 months) | Moderate (6–12 months) |

Strategy 6: Engage Your Supply Chain Partners as Intelligence Sources

Your authorized distributors aren't just order-takers — they have visibility into allocation pipelines, factory schedule updates, and cross-customer demand patterns. Establish regular (monthly or quarterly) supply reviews with your distributor FAEs to:

- Get early warning on allocation changes

- Understand where your orders sit in the priority queue

- Identify upcoming flexibility windows for accelerated delivery

- Access distributor-held consignment or bonded stock programs

Kintex-7 Supply Forecast: When Will Lead Times Normalize?

Based on the structural factors analyzed above, here's our forecast for Kintex-7 supply trajectory:

Chart summary: Lead times are forecasted to remain at 22–31 weeks through H1 2026, gradually improve to 18–24 weeks in H2 2026, and stabilize at 14–20 weeks in H1 2027 as KU+ Gen 2 enters mass production and 7-Series demand begins to plateau.

H1 2026 (Now → June 2026): Lead times remain at 22–31 weeks. No meaningful improvement expected as TSMC continues 28nm capacity rebalancing and 5G/AI demand remains elevated.

H2 2026 (July → December 2026): Gradual improvement to 18–24 weeks. Some demand will begin shifting to UltraScale+ as new designs reach production, reducing pressure on 7-Series allocation.

H1 2027: Stabilization at 14–20 weeks. The launch of Kintex UltraScale+ Gen 2 will accelerate new-design migration away from 7-Series, further easing supply pressure. However, lead times are unlikely to return to pre-shortage levels (~8–12 weeks) because TSMC's 28nm capacity will be structurally smaller.

Our candid assessment: Kintex-7 FPGAs will remain a "plan ahead" category for the foreseeable future. The combination of permanent 28nm capacity reduction at TSMC, sustained end-market demand, and AMD's portfolio prioritization means that the old world of 8-week lead times and abundant shelf stock is not coming back for this product family.

The Bottom Line

The XC7K325T-2FFG900I isn't going away — AMD has committed to supporting it through at least 2040. But "supported" doesn't mean "easy to buy." The underlying supply dynamics — constrained 28nm foundry capacity, structurally elevated demand from telecom/defense/industrial/energy markets, and AMD's natural strategic focus on next-generation products — mean that Kintex-7 supply will remain tighter than historical norms for the foreseeable future.

For procurement teams and hardware planners, the message is clear:

- Plan early — 6–12 month forecast horizons, not 8-week cycles

- Source broadly — multiple authorized channels plus vetted independents

- Carry buffer — 2–4 months of safety stock for production-critical FPGAs

- Verify quality — especially for non-authorized channel purchases

- Think forward — evaluate UltraScale+ for next-gen designs to escape the 28nm capacity trap

The teams that treat FPGA procurement as a strategic function — rather than a routine purchase order — will be the ones that avoid supply disruptions and maintain competitive advantage in 2026 and beyond.

Related Resources from icallin.com:

- Browse XC7K325T-2FFG900I inventory and pricing →

- Kintex-7 FPGA family product listings →

- Quality assurance and component inspection services →

Need help sourcing XC7K325T-2FFG900I or other Kintex-7 FPGAs? At icallin.com, we maintain verified inventory of high-demand AMD/Xilinx FPGAs with full traceability, date code documentation, and quality inspection reports. Whether you need 5 units for prototyping or 500 for production, our team can provide current availability, competitive pricing, and flexible logistics.

📧 Get XC7K325T-2FFG900I stock availability and pricing | 🔗 Browse our AMD/Xilinx FPGA inventory